Changes Over the Past Few Years Have Made Our State and Local Tax Code More Equitable

Changes Over the Past Few Years Have Made Our State and Local Tax Code More Equitable

Download this fact sheet (Feb. 2024; 2 pages; pdf)

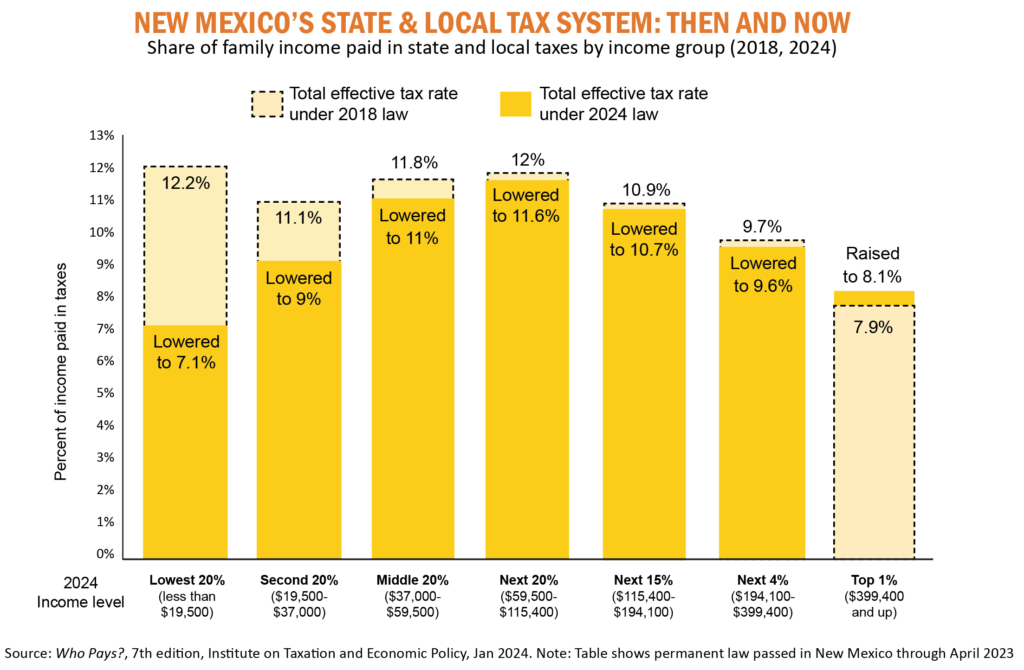

New Mexico now has the ninth most progressive tax system in the nation as ranked by the Institute on Taxation and Economic Policy’s recently updated Who Pays? report on tax incidence. That same report showed New Mexico as making the most progress toward tax fairness in the nation!

Most people agree that low-income households shouldn’t pay a higher percentage of their income in taxes than the rich. But in many states, they do. Most state tax systems are regressive because they rely heavily on sales and property taxes, which hit those earning the lowest incomes the hardest.

New Mexico’s state and local tax code used to be upside-down like this. As shown in the dotted, light yellow bars in the graphic, those who earned the lowest incomes in New Mexico used to pay more than 12% of their income in state and local taxes, while those at the very top paid less than 8%.

That was not only unfair, but it exacerbated income inequality and it was racially inequitable, since people of color are disproportionately more likely to earn lower incomes than white people due to institutional and systemic racism and discriminatory policies in areas such as housing, financing, hiring and the workplace, that have determined who does and does not have access to income and wealth-building opportunities.

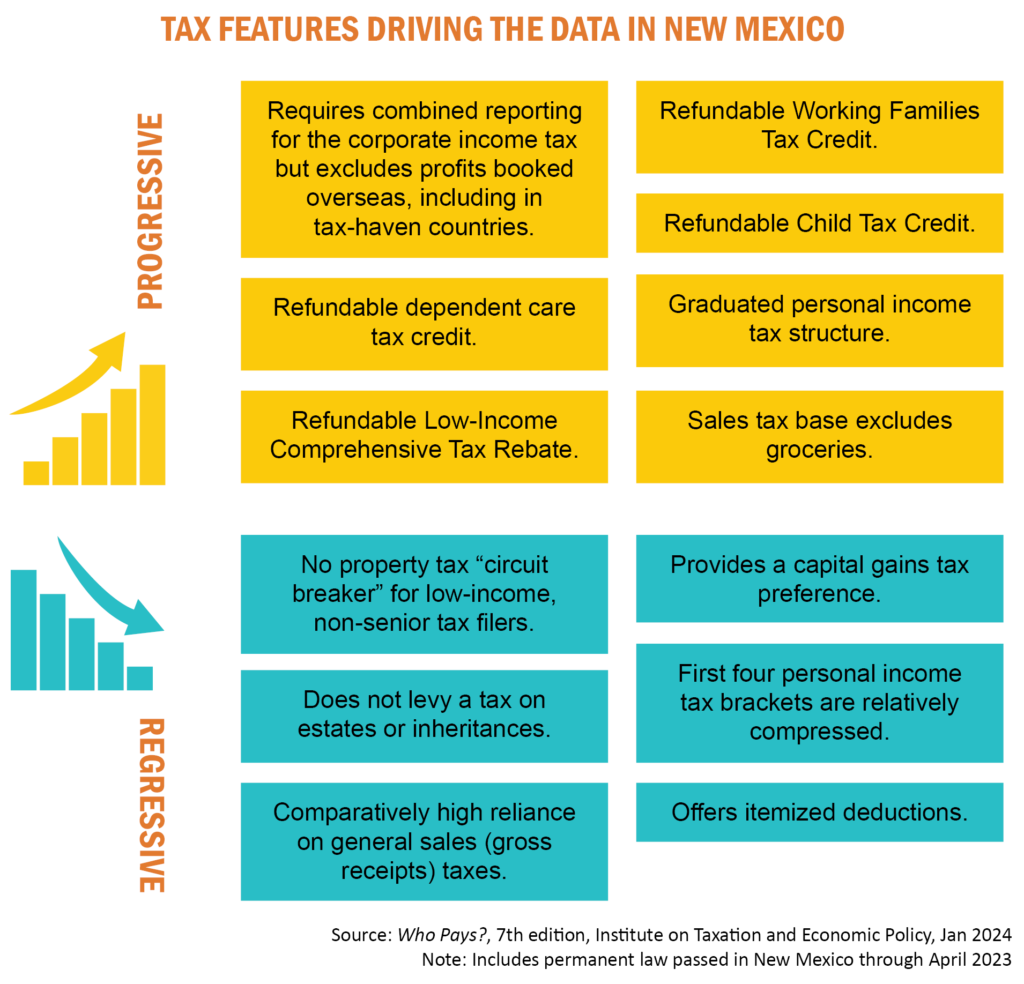

Fortunately, New Mexico’s Legislature and Governor have made many improvements to our tax code (shown in the gold bars on the graphic) that have advanced equity in New Mexico. While lowering rates for almost all income groups, these changes especially improved things for those earning the lowest incomes. These changes included expansions to low-income credits, the creation of a new Child Tax Credit and dependent deduction, and a rate cut to the gross receipts tax. An expanded exemption for Social Security income helped those in the upper-middle income categories, while a reduction to the preference for capital gains income and a new top income tax rate increased the tax rate slightly for those at the very top.

While the tax code is vastly improved for those earning the lowest incomes, there is still work to do to address lingering regressivity at the upper end of the income scale, as those at the very top still pay the next lowest effective rate. We can do that by further reducing the preference for capital gains income and increasing the personal income tax rates for those earning the highest incomes.