Download this policy brief (October 2022; 4 pages; pdf)

Download this policy brief (October 2022; 4 pages; pdf)

By Emily Wildau, MPP

In August 2022, the Biden Administration announced that the COVID-19 pause on student loan payments would be extended for a final time, along with a plan to provide federal student loan debt relief to millions of borrowers. New Mexico has made incredible strides to provide tuition-free access to higher education for everyone in our state, but student debt is still a problem here. Many former students who didn’t have access to tuition-free college are still burdened with loan payment and many current students continue to acquire student loan debt to pay for the non-tuition costs of attendance.

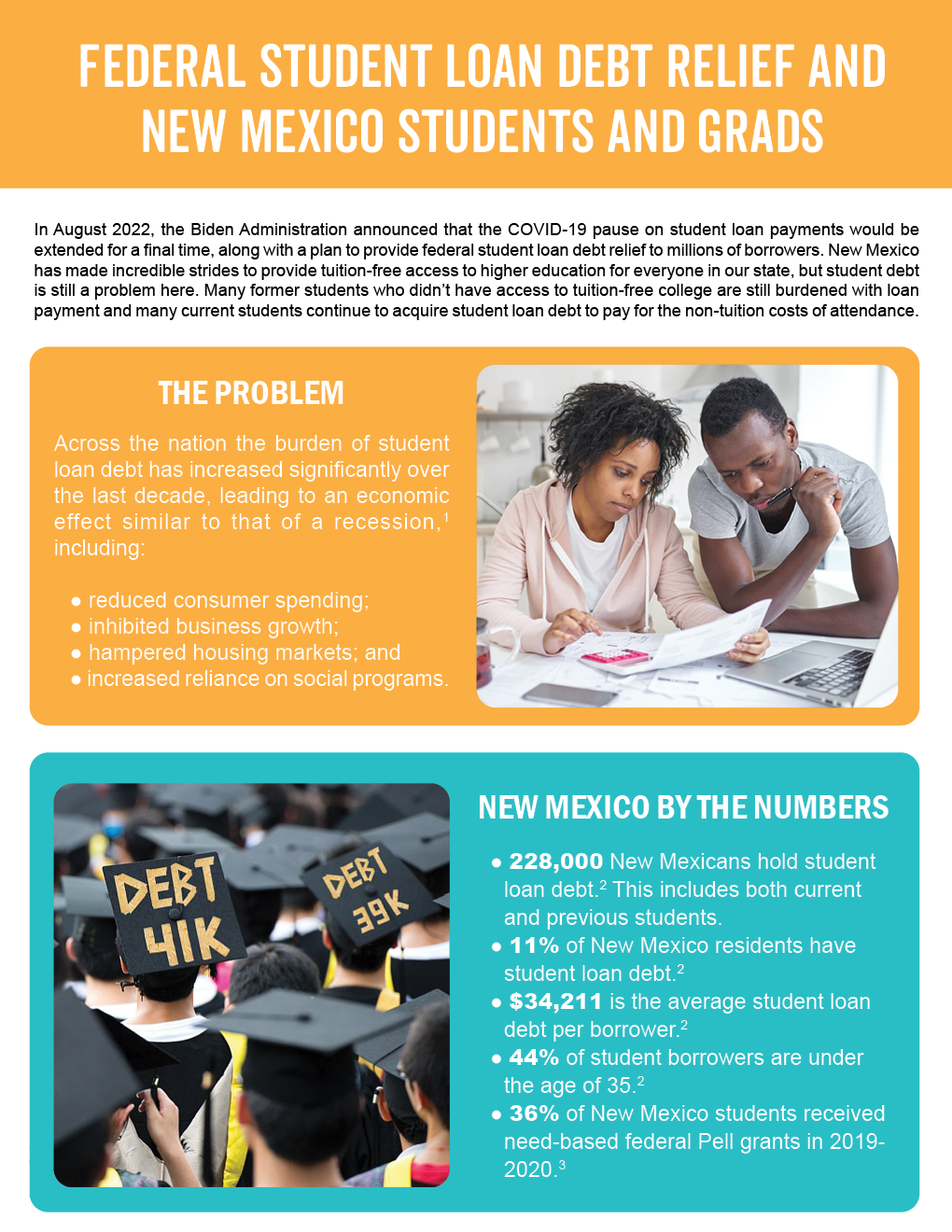

The Problem

Across the nation the burden of student loan debt has increased significantly over the last decade, leading to an economic effect similar to that of a recession,[1] including:

- reduced consumer spending;

- inhibited business growth;

- hampered housing markets; and

- increased reliance on social programs.

New Mexico By the Numbers

- 228,000 New Mexicans hold student loan debt.[2] This includes both current and previous students.

- 11% of New Mexico residents have student loan debt.[2]

- $34,211 is the average student loan debt per borrower.[2]

- 44% of student borrowers are under the age of 35.[2]

- 36% of New Mexico students received need-based federal Pell grants in 2019- 2020.[3]

Disparities by Race

While the vast majority of student debt in New Mexico is held by Hispanic and white students, Native American and Black students are more likely to hold student debt than are students of other races and ethnicities. This disproportionately burdens Native and Black communities.

The Biden Administration’s Student Debt Relief Plan

President Biden’s student debt relief plan could assist an estimated 43 million borrowers nationwide, including 20 million who would have their full balance covered. Nearly 90% of this relief will go to those who have left college and earn less than $75,000 a year.[4] Most borrowers could receive up to $10,000 in federal student loan debt relief. Borrowers who also received Pell Grants while in college could receive debt relief up to $20,000.

Deadlines

Early Oct. 2022 Simple application for Debt Relief opens

Oct. 31, 2022 Last day to apply for full loan forgiveness under temporary changes in eligibility criteria for the Public Service Loan Forgiveness (PSLF) program

Nov. 15, 2022 Last day to apply for debt relief to receive it prior to the expiration of the student loan payment pause

Dec. 31, 2022 Pause on student loan payments ends

Dec. 31, 2023 Last day to apply for student loan debt relief

Who’s eligible

- Individuals who earned less than $125,000 annually, or couples filing jointly and earning less than $250,000 in 2021 or 2020 are eligible.[5]

- Borrowers with Federal Undergraduate and Graduate Stafford Direct, Grad PLUS, consolidation, and Parent PLUS loans are eligible, as are any of these loans that are in default if they originated before July 1, 2022.[6]

- Federal Family Education and Perkins loans held by the U.S. Department of Education (ED) are eligible, but those that are not held by ED are only eligible if the borrower applied to consolidate these loans into the Direct Loan program prior to September 29, 2022.[6]

- Borrowers who also received a full or partial Pell Grant at any point in their education qualifies for up to $20,000 in debt relief.[6]

- Borrowers who did not complete a degree program are still eligible for student loan debt relief.[6]

- Borrowers who are employed by non-profits, the military, or federal, state, Tribal, or local government may be eligible to have all of their student loans forgiven entirely through the Public Service Loan Forgiveness (PSLF) program. But they must apply by October 31, 2022, which is when temporary changes that waive certain eligibility criteria expire.[7]

How the Student Loan Debt Relief Plan works[7]

- The COVID-19 federal loan payment pause is automatically extended for a final time until the end of this year. Student loan relief will become available for some borrowers as soon as November before loan repayments begin. This timing is intended to decrease loan defaults for borrowers with the highest risk of delinquency.

- Relief is capped at the amount of outstanding debt an eligible borrower holds. Borrowers will not receive additional rebates to equal the total maximum amount for which they were eligible. For example, if a borrower is eligible for up to $10,000 in relief but holds a loan balance of $4,000, that borrower will see their $4,000 balance forgiven, while a similar borrower with a loan balance of $12,000 would receive $10,000 in relief and still hold a balance of $2,000.

- An estimated 8 million borrowers may receive relief automatically because relevant income data is already available to the U.S. Department of Education. Borrowers will be notified by email and/or text message if they automatically qualify.

- For those who don’t automatically qualify, a simple application will be made available through the Department of Education beginning in October of 2022. Borrowers should apply before November 15, 2022, to receive relief before the COVID-19 loan payment pause expires on December 31, 2022.

- After completing the simple application, a borrower can expect relief within 4 to 6 weeks.

- All who are eligible for student loan debt relief have until December 31, 2023, to apply for relief.

Changes to Income-Driven Repayment plans[7]

Currently, any borrower with eligible loans can apply for an Income-Driven Repayment (IDR) plan to pay off student loans. IDR plans set a monthly payment rate for borrowers based on their income and family size to make payments more affordable. Repayment periods range from 10 to 25 years. As long as borrowers continue to make payments under their IDR plan, any balance remaining at the end of the repayment period qualifies for debt relief.[8] The student loan debt relief plan will create a new, more generous IDR plan to further increase payment affordability for future federal loans that won’t qualify for relief and for many loan balances remaining after relief in the following ways:

- Payment amounts will be set based on a lower share of discretionary income. This will further reduce monthly payments for low- and middle-income borrowers from the current 10% of their discretionary income to 5%.

- A new rule will guarantee that no borrower earning less than 225% of the federal poverty level – about the equivalent of a $15 an hour wage for an individual – will have to make monthly payments.

- Borrowers with original loan balances of $12,000 or less will have their remaining balance forgiven after 10 years instead of 20, a change that is expected to allow nearly all community college borrowers to be debt-free within 10 years.[9]

- Under the current IDR plans, loans continue to accrue interest so balances grow significantly – ultimately increasing borrower debt. Now, unpaid monthly interest will be covered to prevent loan balances from growing as long as borrowers make their monthly payments, even if they have a monthly payment of $0 – effectively forgiving unpaid monthly interest so the total a borrower owes can’t rise above the starting balance.[10]

How New Mexico Can Leverage Student Loan Debt Relief

The Biden Administration’s student loan debt relief plan is a step toward alleviating the significant debt burden of student borrowers, allowing more New Mexicans to thrive, and strengthening our economy. To make the plan even more meaningful for New Mexico borrowers, our policymakers can:

- provide more need-based financial aid for the costs of attendance beyond tuition; and

- fully fund child care assistance, increase the state’s Child Tax Credit, and increase funding for cash assistance and other programs that help students with children pay for basic living expenses while they attend school.

[1] Economic Effects of Student Loan Debt, Education Data Initiative, April 2022

[2] Student Loan Debt by State, New Mexico, Education Data Initiative, April 2022

[3] Student Financial Aid Data, Integrated Postsecondary Education Data System (IPEDS), National Center for Education Statistics, U.S. Department of Education, 2019-2020

[4] Here’s everything you need to know about Biden’s latest student loan system changes, Higher Ed Dive, August 2022

[5] “What You Need to Know About Biden’s Student Loan Forgiveness Plan,” New York Times, August 2022

[6] One-Time Student Loan Debt Relief, Federal Student Aid, U.S. Department of Education, August 2022

[7] The Biden-Harris Administration’s Student Debt Relief Plan Explained, Federal Student Aid, U.S. Department of Education, August 2022

[8] “If your federal student loan payments are high compared to your income, you may want to repay your loans under an income-driven repayment plan,” Federal Student Aid, U.S. Department of Education

[9] “Fact Sheet: President Biden Announces Student Loan Relief for Borrowers Who Need It Most,” White House, Aug. 24, 2022

[10] Ibid