The Martinez Administration’s “37” Tax Cuts

by Raphael Pacheco, MBA

by Raphael Pacheco, MBA

March 22, 2017

As the 2017 regular legislative session ends, New Mexico finds itself in familiar territory—with no money in a slow-moving economy. The same tired rhetoric of no tax increases—a pledge made by Governor Susana Martinez since she has taken office—has led to deep cuts in essential services like education, public safety, and health care.

Because we often hear the administration touting the 37 tax cuts made since Governor Richardson left office in 2011, obviously the executive believes we can cut our way to prosperity. But in reality, these cuts helped put our state in the red.

All tax cuts serve a fundamental purpose—to change behavior. For example, if you were able to deduct all purchases you made on pizza from your personal income taxes every year, you would probably eat a lot more pizza. That logic is valid for a tax cut on jet fuel enacted by the Martinez administration in 2011. By reducing taxes on jet fuel, it is hoped that more jet fuel is purchased in New Mexico, thus resulting in an economic boost to the airline industries. This isn’t the problem.

The problem occurs when the underlying assumption for a behavior change is incorrect. In 2014, the Martinez administration passed a tax deduction for the sale of infusion therapy services. Infusion therapy is the practice of administering medication through needles or catheters. What behavior was this tax cut aimed at changing? Not the behavior of the service providers. They weren’t going to leave the state because the cost of doing business was too high. These services were going to stay in New Mexico because the demand for them is high. It won’t change the behavior of consumers because these are likely life-saving services. And, due to an aging population, the Affordable Care Act, and expanded access to Medicaid, more people need and can afford these services.

But even if the underlying assumption is correct, at least on paper, a different problem may occur. Going back to the jet fuel example: in the five years since the tax cut was implemented, it is unclear if the deduction is having any influence on purchases of jet fuel in New Mexico, according to the 2016 tax expenditure report. So if the tax cuts are not resulting in the intended outcome motivated by the assumption, or the underlying assumption was just flat incorrect, then they are not working. Put simply, if tax cuts are ineffective, we should not still have them in the tax code.

This brings me to another problem. If these tax cuts have minimal impacts on job creation and industry growth while simultaneously leaving New Mexico in a bigger fiscal hole than we were in before, why do we keep them? When will we change strategies?

Death by 37 (tax) cuts

A blog by Capitol Report New Mexico outlined the few dozen tax cuts the governor has claimed to have made during her tenure. I wanted to dig deeper into these tax cuts to see how much they cost and if they benefited the state. After several hours of poring through fiscal impact reports and legislation, several hundred milligrams of caffeine, and about five Excel spreadsheets later, I now present to you the 37 (29 is probably more accurate) tax cuts provided by the Martinez administration.

Before diving in, I ask the reader to realize that, for me, researching tax policy is best described by the blue line in Figure I. While, for you, interest may by graphed more like the orange line.

Frankly, the phrase “getting into the weeds” doesn’t do this research justice. So to spare some of your time and sanity, I won’t go into detail for every tax cut the administration claims as their own. If you’re interested in learning more about any of these cuts, however, please feel free to email me.

Let’s dig in!

2011 Regular Legislative Session

HB 273 Small Business Tax Credit Eligibility Period cost: $761,000

Do you own a small business? If not, you didn’t benefit from this cut that ended in the summer of 2015. This bill extended the eligibility period for the Research and Development Small Business Tax Credit. Not a large number of taxpayers, however, were eligible for this credit. It’s simply targeted legislation that helps a select few, a pattern that will continue as we work our way through the years.

HB 440 Advanced Energy Tax Deduction for Some Leases cost: $44.2 million

Although the current administration claims this deduction as their own, HB 440 was merely an extension of a tax cut enacted by the Richardson administration—the Advanced Energy Gross Receipts Tax Deduction for the sale of “equipment for an advanced electrical generation facility.” If you’re asking yourself what that means for you and me, the answer is “not much.” The Martinez extension added “leases” in addition to sales and purchases of eligible electrical equipment. And for most New Mexicans this is much ado about nothing.

HB 523 & SB 179 Locomotive Fuel Gross Receipts Deduction cost: $19.5 million

Remember this one? This was dubbed the “Union Pacific” bill by many because it made locomotive fuel tax exempt, contingent upon Union Pacific opening a port in Doña Ana County, specifically Santa Teresa. Union Pacific has been cited as saying that the bill allowed for the construction of the facility, so we’ll take their word for it and give the administration the benefit of the special-interest doubt on this one.

SB 84 Jet Fuel Gross Receipts cost: $4.4 million

This is the jet fuel tax reduction mentioned before for fuel prepared and sold for use in turboprop or jet-type engines. And we still don’t know if it helped the airline industry in New Mexico.

SB 282 Tax Liability for Certain Physicians cost: $275,000

Are you a clinical oncologist in rural New Mexico who treats patients in cancer clinical trials? You may start to get the pattern by now, but you almost certainly didn’t get the tax cut.

Will the remaining years be any better? Keep in mind we’re only a fifth of the way through!

2012 Regular Session

HB 10 Veteran Employment Tax Credit cost: $12 million

This bill allowed business owners in New Mexico to receive a $1,000 tax credit for each veteran they hire. This credit brings up an interesting problem. By creating a tax preference for hiring veterans, it places non-veteran job applicants at a disadvantage. Additionally, there is no consensus on whether veterans have significantly different unemployment rates than other groups of men, for example, in those age ranges. To illustrate, the unemployment rate for Gulf War-era veterans is 4.8 percent which is only slightly higher than the nationwide average for men aged 35 to 44.[1] For additional comparison, the state’s unemployment rate is 6.7 percent.

HB 116 Electric Conversion Facility Gross Receipts cost: unknown

This law provided a tax exemption for the electricity that is used during the production and transmission of electricity. Simply put, it’s a tax break for getting power from point A (like a power grid) to point B (like homes or businesses). The purpose of the exemption was to encourage the building of power lines and to provide an incentive for an electricity exchange to be located in New Mexico. (Although no fiscal impact report was done for this bill, it’s estimated[2] that for an energy company with sales of $500 million, the state would lose $29 million per year.) Despite the cost, this puts us in line with other state’s tax structures.

HB 184/256 Construction Service for Gross Receipts & Manufacturing Property Gross Receipts cost: almost $200 million

These tax deductions are the most glaring of all. Costing the state almost $200 million in lost revenue since their creation, the two deductions are directly counter to the Legislative Finance Committee tax policy principle of adequacy, which means it will cost more to implement this tax change than it’s worth.

The first of these, the Manufacturing Gross Receipts Deduction, allows the deduction of “property consumed in the manufacturing process”—or the cost of the stuff used in the making of other stuff. This would include the cost of utilities, for example. The intention of this legislation was to reduce pyramiding. This means taxes charged on business-to-business sales that become embedded as part of the cost and thus making the final product more expensive.

The second, the Construction Gross Receipts Deduction, makes it easier for a construction worker to rent equipment without having to pay tax on it.

It was hoped that these would create more jobs in the manufacturing and construction industries. Although job creation is not included in the impact analysis, when the deductions went into effect in 2013, there were 28,800 workers in the manufacturing industry in New Mexico; that number is now at 26,500—a decrease of 8 percent. Construction, however, was at 40,100 workers at the beginning of 2013 and that number is now 45,200—an increase of 12.7 percent. Together, we have a net gain of 2,800 jobs in these two industries over four years. So, essentially, the state spent $70,000 for each of these jobs, which is likely more than these jobs pay. This assumes, however, that all jobs can be attributed to the exemption—clearly, employment in this industry can be attributed to other factors not related to this deduction as well.

SB 32 Temporary Unemployment Fund Contributions cost: $160 million

This bill changed the amount of money employers had to pay into the unemployment insurance trust fund, which compromises the fund’s solvency. Will the fund be solvent for the next economic down-turn? I’m skeptical. It’s also not a tax cut so much as an insurance rate cut.

2013 Regular Session

HB 106 Increase Value of City Property for Lease cost: negligible

This bill raises the threshold from $25,000 to $250,000 for the sale of municipally owned facilities or real property without a referendum (a vote by the electorate). It might save some time, but it’s not a tax cut.

HB 641 Film Production Tax Credit Changes cost: $68.8 million

Truly a Barnum & Bailey bill, this bill made several changes to the tax code and not to just the film industry. HB 641 did seven things but here are the worst:

- Lowered the corporate income tax rate over five years;

- Allowed manufacturing corporations to not pay any income tax; and

- Allowed municipalities and counties to increase their local tax rates.

Let’s see here: a cut for corporations, another cut for corporations, and a tax hike for the rest of us. You and I foot the bill at almost $69 million. Sounds fair.

SB 81 Liquor Tax Microbrew Volume Limit cost: $2.3 million

Tax bills about beer? Finally! Truly a bill after my own heart, this amended the language and definition of what constitutes a microbrewer. It now means a brewer who produces fewer than 15,000 barrels of beer annually, whereas the threshold was less than 5,000 barrels before. This allowed more brewers to qualify for the credit, as well as lowered the tax rate of microbrewed beer from 41 cents to a mere 8 cents (for the first 10,000 gallons). In New Mexico we have enjoyed the prosperity of craft microbreweries for a while now. As the market has experienced a massive increase in patronage as millennials continue to age and imbibe, tax cuts for burgeoning industries are often sound tax policy. But an 80 percent tax decrease on brews produced—do microbrewers really need that much help?

SB 116 Liquor Tax Small Winegrowers Volume Limit cost: $1.8 million

If beer isn’t your thing, perhaps wine is. This bill increased the production cap for small winegrowers as well as cut the tax rate for each liter of wine produced within in that new range from 45 cents to 30 cents. Now again, there is nothing wrong with cutting taxes to spur industry growth. Please keep in mind, however, this is a tax cut for winegrowers, not the people who drink wine. And much like the microbrewery bill before, this cut decreased state revenues, which in the end means less access to vital services for you and me.

SB 160 New Biodiesel Definitions cost: $2.3 million

There are exactly two producers in New Mexico that make the biofuel that falls under this definition: Rio Valley Biofuels and Renewable Energy Group, located in Anthony and Clovis, respectively. SB 160 is a tax cut tailored for these producers. At the time of the analysis a third producer existed but had not yet begun production.

2014 Regular Session

HB 14 Aircraft Parts & Maintenance Gross Receipts cost: $1.6 million

This bill provides a tax deduction for selling aircraft parts or maintenance services for aircraft or aircraft parts. A cut for aviation but not for me and you.

SB 88 Infusion Therapy & Medical Supply Gross Receipts cost: $8.9 million

We’ve already looked at this tax deduction for the sale of infusion therapy so there’s not much more to say except that when the legislation was enacted there were 40 infusion therapy equipment suppliers who filed gross receipts tax returns which suggests that this is an industry likely to thrive without special treatment.

HB 32 Dialysis Facility Service Gross Receipts cost: $3.7 million

A similar type of legislation was also passed in 2014 that provided a tax deduction for health services provided by a dialysis facility to Medicare beneficiaries. About 3,000 dialysis patients reside in New Mexico so this is a deduction that benefits only a few. The real problem is that both this deduction and the infusion therapy deduction exist in markets that are driven by demand, meaning they will likely continue to succeed as long as people need the services. These kinds of tax deductions should only be used to encourage the supply side of the equation (such as beer and wine consumption).

2015 Regular Session

SB 279 Sustainable Building Tax Credits cost: $10 million

This bill was enacted in 2013 and amended in 2015. The credit was designed to be used for the construction and renovation of either commercial or residential buildings that met the “LEED green build rating system.” Investing in green infrastructure is something everyone can get behind and hopefully this credit will actually serve its purpose for constructing higher quality buildings and encouraging energy efficiency.

SB 506 Disabled Veteran Property Tax Exemptions cost: negligible

This legislation enables disabled veterans to maintain their exemption on property tax even if they change their residence. This does not qualify as a tax cut and the fiscal impact is negligible.

2015 Special Session

The 2015 Special Legislative Session resulted in a tax package that contained a lot of moving parts but little in the way of tax cuts for New Mexico’s hard-working families.

HB 2 Angel Investment Tax Credit cost: $1.3 million

A tax cut for investors. The term “angel” refers to an individual who provides capital for start-up business costs in exchange for some equity in the business or convertible debt.

HB 2 Singles Sales for CIT and Border Zone Trade for GRT combined cost: about $200,000

With a combined loss of a little over $200,000 to state revenues—very little money in the scheme of things—it is difficult qualifying these as additional tax cuts.

HB 2 US Department of Defense Energy GRT cost: $9.3 million

The Air Force Research Laboratory (AFRL) at Kirtland Air Force Base is the primary recipient of this tax break. In February 2015, UNM’s Bureau of Business and Economic Research concluded that the economic impact of the AFRL was $536 million, so a $9.3 million impact seems relatively small and justified if it keeps them in New Mexico.

HB 2 Tech Jobs and R&D Tax Credit cost: $5.2 million

The stated purpose of this legislation is to provide a favorable tax climate for technology-based businesses engaging in research, development, and experimentation to promote increased employment and higher wages in these fields. Recent data show that 54,577 New Mexicans were employed in the Professional, Scientific, and Technical Service Industry in New Mexico in 2015 with an average wage of $1,445 a week.

Where does that leave us in 2017?

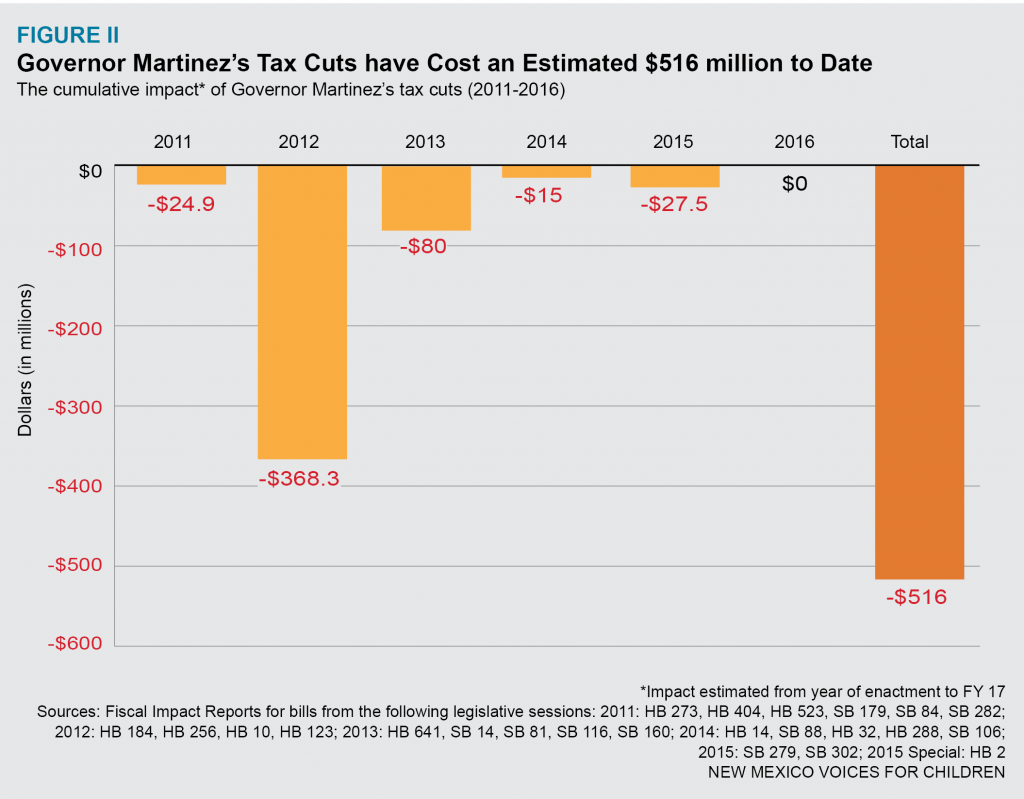

The tax cuts heralded by Susana Martinez have cost the state more than $500 million during her stay as governor of New Mexico (see Figure II). Frankly, the 37 cuts figure the Martinez administration often references is inflated and misleading. But regardless if the number is 1, 29, 37, or 500 million, when will the special interest tax breaks end?

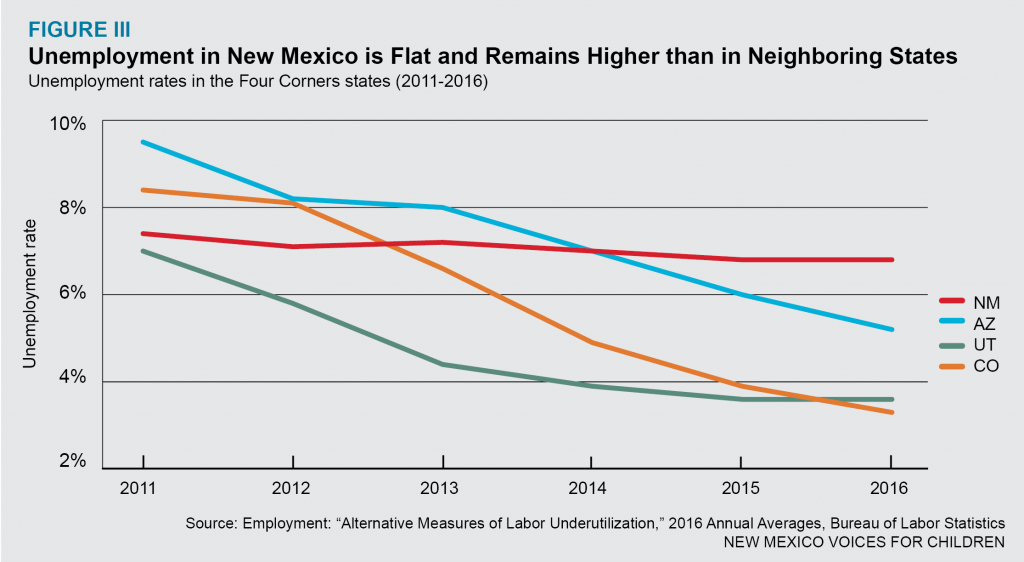

Did the tax cuts have their hoped-for job-creating impact? That’s hard to say, but I leave you with Figure III so you may make your own conclusions (and, no, the state’s unemployment rate hasn’t gotten better since 2016. In fact, in January of 2017 it was 6.7 percent—the highest in the nation).

Dear reader, whether good or bad, for you or not, tax cuts that are not offset with new revenue are irresponsible and regrettable at best and off-target and unsustainable at worst. We must restore lost revenue to the state if we are to survive another fiscal year. The first rule about getting out of a hole if you find yourself in one, is to stop digging. A hole filled with half a billion one-dollar bills is about 63 cubic meters by volume. It’s time to stop digging.

[1] https://www.bls.gov/news.release/vet.t01.htm, table 1 employment status of veteran by veteran status, May 2016

[2] Fiscal Impact Report, Electric Conversion Facility Gross Receipts, Legislative Finance Committee, February 2012

Raphael Pacheco, MBA, is a Research and Policy Analyst and the State Priorities Partnership Fellow for NM Voices for Children.